Published on : 06 Jan 2026

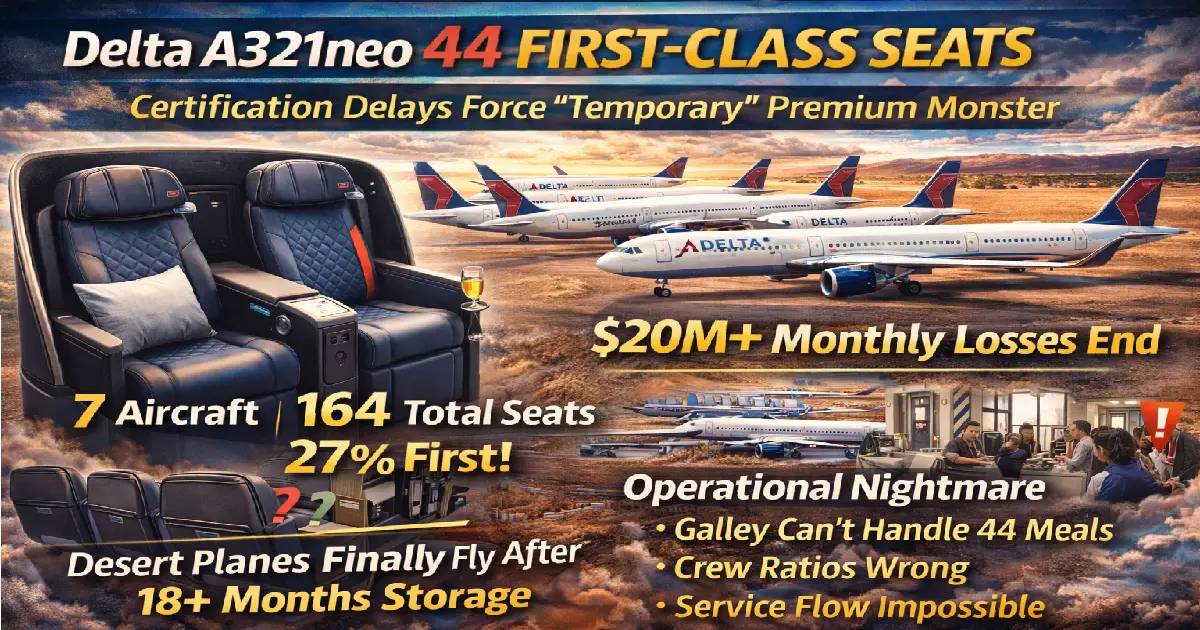

Breaking: Delta Air Lines deploys unprecedented Airbus A321neo configuration summer 2026—44 first-class seats (vs standard 20) representing 27% total cabin capacity (highest premium percentage US narrowbody history), temporary solution addressing $20M+ monthly costs parking factory-fresh aircraft delivered October 2024-present in desert storage awaiting Safran Vue lie-flat business class seat certification still pending 18+ months post-delivery. Up to 7 aircraft entering service this “limited edition” interim layout: 44 first (11 rows!), 54 Comfort+ extra-legroom, 66 standard economy = 164 total (vs standard 194-seat A321neo)—shrinking plane by 30 seats to accommodate doubled premium cabin generating 3-4× revenue per square foot targeting transcontinental/high-business routes (JFK-LAX potentially, though Delta hasn’t confirmed) where corporate travelers book first regardless of price + Medallion elites expect upgrade availability. PROBLEM: Galleys designed for lie-flat configuration can’t support 44 premium meal services (equipment insufficient, storage limited, crew workflow impossible)—Delta likely serving room-temperature meals OR drastically simplified catering vs traditional hot first-class service, raising question whether passengers accept degraded product despite “first class” ticket prices $600-1,200 one-way domestic. Certification delays stem from Safran Vue seat complexity (doors, electronics, lie-flat mechanics require extensive FAA testing) plus supply chain constraints affecting multiple airlines (United, Lufthansa also experiencing similar delays different seats)—Delta’s original transcontinental premium plan: 16 Delta One lie-flat, 12 Premium Select, 54 Comfort+, 66 economy = 148 ultra-premium config NOW impossible until 2028 earliest (industry insiders estimate), forcing “temporary” 44-first solution potentially lasting 24-36 months (not short-term as Delta publicly suggests). Competitive implications: Largest premium narrowbody undermines JetBlue’s Mini Mint strategy (your article), proves American’s Chicago expansion premium focus correct (your article), validates industry-wide shift toward “quality over quantity” where economy passengers subsidize premium cabin creation—but operational challenges (service flow, crew ratios, turnaround times longer) may demonstrate upper limits of premium-heavy configurations, answering question: How many first-class seats can narrowbody handle before operational costs outweigh revenue benefits?

Published: January 6, 2026 Entry Into Service: Summer 2026 (June-August) Aircraft Affected: Up to 7 Airbus A321neos Configuration: 44 first class, 54 Comfort+, 66 economy = 164 total Standard Configuration: 20 first class, 60 Comfort+, 114 economy = 194 total Premium Percentage: 27% (44/164) vs 10% standard (20/194) Delivery Dates: October 2024-present (sitting in desert storage 12-18+ months)

The Problem:

Delta Air Lines ordered premium A321neo subfleet for transcontinental routes—21 aircraft with ultra-premium 148-seat layout:

The Reality:

Aircraft delivered from Airbus without seats installed—galleys prepared for lie-flat config but Safran Vue seats NOT certified by FAA. Planes parked in desert storage facilities (Victorville, Mojave) generating ZERO revenue while Delta pays:

Total monthly cost per grounded aircraft: ~$300,000-400,000

Up to 7 aircraft grounded: $2.1-2.8 million monthly burn rate = $25-34 million annually for planes sitting idle.

Delta’s Solution:

Rather than continue paying storage costs indefinitely waiting for Safran Vue certification (which may not happen until 2028), Delta installing standard domestic first-class recliners (Recaro seats, same as existing A321neo fleet) in space originally reserved for lie-flat business class.

Result: 44 first-class seats—most premium-heavy narrowbody in US history.

NEW “Temporary” Layout:

| Class | Seats | Rows | Percentage |

|---|---|---|---|

| First Class | 44 | 11 | 27% |

| Comfort+ | 54 | ~9 | 33% |

| Economy | 66 | ~11 | 40% |

| TOTAL | 164 | ~31 | 100% |

Standard A321neo Layout (Comparison):

| Class | Seats | Rows | Percentage |

|---|---|---|---|

| First Class | 20 | 5 | 10% |

| Comfort+ | 60 | 10 | 31% |

| Economy | 114 | 19 | 59% |

| TOTAL | 194 | 34 | 100% |

1. PREMIUM EXPLOSION:

2. CAPACITY LOSS:

3. COMFORT+ SLIGHTLY REDUCED:

4. ECONOMY DRAMATICALLY REDUCED:

Manufacturer: Recaro (German seat supplier)

Specifications:

Amenities:

NOT Included:

Essentially: Identical product to existing A321neo first class—just 2.2× more seats.

Delta hasn’t confirmed specific routes (saying only “more details in 2026”), but aviation analysts speculate:

1. TRANSCONTINENTAL:

Why: Long-haul domestic = highest first-class demand (corporate travelers willing to pay $800-1,500 one-way vs $250-400 economy). Delta currently flies widebodies (A330, 767) on these routes—A321neo with 44 first seats offers similar premium capacity narrowbody economics.

2. HIGH-BUSINESS CORRIDORS:

Why: Routes with consistent first-class demand year-round (not just seasonal peaks).

3. LEISURE HOTSPOTS (Lower Probability):

Why: Leisure travelers LESS willing to pay first-class premiums—44 first seats may be overkill unless targeting high-rollers/conventiongoers.

Standard 194-Seat A321neo (JFK-LAX example):

NEW 164-Seat “44 First” A321neo (JFK-LAX example):

Difference: +$7,500 per flight (+11% revenue)

7 aircraft with 44-first config:

1. LOAD FACTOR ASSUMPTIONS:

2. FARE ELASTICITY:

3. OPERATIONAL COSTS:

Galleys designed for lie-flat business class—NOT 44 domestic first meals.

Lie-flat config (original plan):

44-first config (actual reality):

Delta’s Solutions (Speculative—Not Officially Confirmed):

Option A: Room-Temperature Meals

Option B: Simplified Service

Option C: Multi-Course Cart Service

FAA Minimum: 1 flight attendant per 50 passengers

164-seat plane: 4 flight attendants minimum (same as 194-seat standard)

BUT:

Service demands:

Result: Service degraded—passengers notice, complain, Delta reputation suffers.

Standard A321neo:

44-first A321neo:

Result: Turnaround time 40-50 minutes—reduces aircraft utilization (fewer daily flights = less revenue).

Features:

Why Complex:

October 2024: First A321neo delivered WITHOUT seats (empty business class section)

Expected Timeline (Original):

Actual Timeline:

Industry Insiders Estimate:

Why Delays:

2020-2024 Investments:

2025 Financial Results:

American Airlines (Your Article Covered):

United Airlines:

JetBlue (Your Article Covered):

Southwest (Your Articles Covered):

Conclusion: ALL carriers pursuing SAME strategy—monetize premium, squeeze economy.

Delta’s Official Statement:

“Select A321neo aircraft are expected to begin their entrance into service next year with an updated seat configuration designed with comfort in mind. We look forward to sharing more in 2026.”

Translation: “We have no idea when Safran Vue seats will be certified, so we’re calling this ‘temporary’ to avoid admitting it might be 2+ years.”

Realistic Timeline:

Best Case: 18-24 months (mid-2027 to end-2027)

Likely Case: 24-36 months (mid-2028)

Worst Case: 36+ months (2029+)

Good News:

Bad News:

Bad News:

Good News:

But:

Delta Air Lines’ summer 2026 deployment of Airbus A321neo aircraft with unprecedented 44 domestic first-class seats (27% total cabin vs industry-standard 10%)—up to 7 planes entering service after 18+ months desert storage awaiting Safran Vue lie-flat seat certification still pending 2028 arrival—represents aviation industry’s boldest premium-heavy narrowbody experiment, testing upper limits of how many premium passengers single aircraft can viably serve before operational costs (galley limitations forcing room-temperature meals, crew ratios 11 premium passengers per flight attendant straining service quality, turnaround times extended 10-20 minutes reducing daily utilization) outweigh revenue benefits ($16.4M annual incremental per aircraft assumes 100% first-class occupancy unrealistic given supply doubling 20 → 44 seats potentially depressing fares through oversupply).

“Temporary” designation dubious given certification delays affecting Safran, United, Lufthansa suggest FAA approval unlikely before 2027-2028 (2+ years away), meaning 44-first configuration could persist through 2027-2028 despite Delta publicly framing as short-term stopgap—reality: $25-34M annual storage costs burning cash plus opportunity cost lost revenue forced Delta’s hand deploying incomplete aircraft with band-aid solution rather than indefinite desert parking, betting premium revenue surge (industry trend: Delta premium exceeds economy first time 2025, validating “quality over quantity”) justifies operational headaches even if passenger experience degraded versus traditional first-class service standards.

Competitive implications connect directly to broader industry transformation: JetBlue Mini Mint cutting economy legroom 32″ → 30″ to create first class (your article), Southwest ending open seating introducing premium tiers (your articles), American Chicago expansion premium focus (your article)—Delta’s 44-first A321neo most extreme manifestation of airlines abandoning egalitarian models favoring tiered revenue extraction where economy passengers subsidize premium cabin creation regardless of operational viability, answering fundamental question: Can airlines profitably operate narrowbody with 27% premium seats, or does service quality collapse under operational constraints demonstrating practical limits of premium-heavy configurations future airline executives must heed?

For travelers, summer 2026 offers unprecedented first-class availability (44 seats = easier bookings, better upgrade odds Medallion elites) BUT degraded experience likely (cold meals, slower service, crowded premium feel) raising question whether Delta maintains $900-1,200 first-class fares if product quality suffers—early passenger reviews critical: IF customers complain loudly about inferior service despite “first class” premium, Delta faces choice: Accept reduced margins deploying more crew/better galleys (eroding $16.4M annual revenue benefits), OR maintain current operations accepting reputational damage from disappointed premium passengers who expected traditional first-class experience received budget-premium hybrid instead.

Long-term verdict depends on Safran Vue certification timeline: IF completed 2027-2028 as optimists predict, 44-first config becomes footnote—interesting experiment, temporary solution, aviation trivia. IF delays extend beyond 2028, Delta may retrofit aircraft with DIFFERENT seats (abandoning Safran entirely), making 44-first configuration semi-permanent unintended legacy of certification failures exposing fragility complex premium seat designs where doors, electronics, lie-flat mechanics create regulatory nightmares delaying aircraft entries 18-36 months costing airlines hundreds of millions in storage fees plus lost revenue—cautionary tale for airline executives betting on cutting-edge seat technology without proven certification track records.

Related Travel Tourister Coverage:

Published: January 6, 2026 Last Updated: January 6, 2026 at 3:00 PM ET Reading Time: 45 minutes

Posted By : Vinay

This article is provided for general informational purposes only and is based on information available at the time of publication. Travel advisories, airline schedules, airport operations, visa requirements, government regulations, and other travel-related information are subject to change without prior notice. While Travel Tourister makes reasonable efforts to verify information using official announcements, government publications, airline and airport communications, and other reliable sources, we cannot guarantee that all information remains complete, accurate, or up to date at all times. Readers should independently verify any information that may affect their travel plans with the relevant airline, airport authority, government agency, embassy, or other official source before making travel, financial, or other decisions. Travel Tourister shall not be liable for any direct or indirect loss, inconvenience, or damages arising from the use of or reliance on the information contained in this article. Nothing in this publication constitutes legal, immigration, financial, or professional travel advice. If you believe any information in this article is inaccurate or outdated, please contact our editorial team. We review all credible correction requests promptly and update our content whenever appropriate.

Lastest News

2nd Floor, 39, Above Kirti Club, DLF Industrial Area, Kirti Nagar, New Delhi, Delhi 110015

Travel Tourister is a leading Travel portal where we introduce travellers to trusted travel agents to make their journey hasselfree, memorable And happy. Travel Tourister is a platform where travellers get Tour packages ,Hotel packages deals through trusted travel companies And hoteliers who are working with us across the world. We always try to find new and more travel agents and hoteliers from every nook and corners across the world so that you could compare the deals with different travel agents and hoteliers and book your tour or hotel with the one you have chosen according to your taste and budget.

Copyright © Travel Tourister, India. All Rights Reserved

Call

Call Enquiry

Enquiry