Published on : 17 Jun 2026

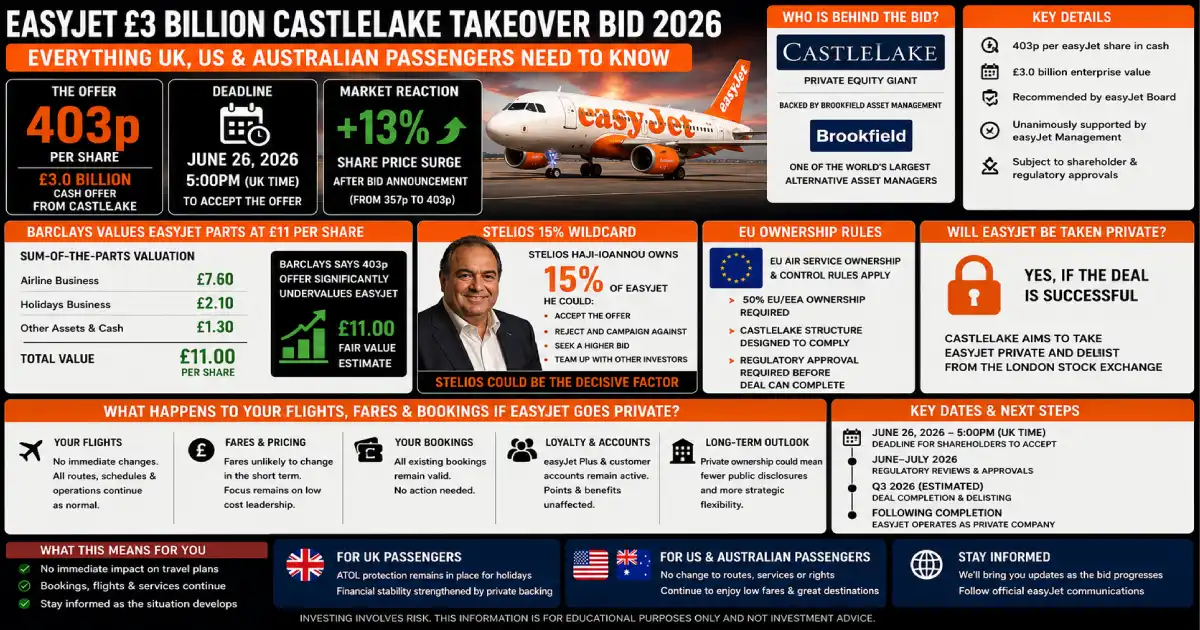

Published: June 17, 2026 — (9 Days to June 26 Deadline) Status: Possible offer period — NOT a confirmed bid Bidder: Castlelake L.P. — Minneapolis, Minnesota — majority owned by Brookfield Asset Management Target: EasyJet plc — Luton, Bedfordshire — Europe’s second-largest low-cost carrier Bid announcement: May 29–June 1, 2026 — “early stages of considering a possible offer” Current stake: Castlelake holds 16,241,494 easyJet shares — 2.14% of issued share capital Minimum bid price stated: 403.23 pence per share — values easyJet equity at minimum £3.06 billion Share price reaction: Surged as much as +13% to 449.9p on announcement — valuing easyJet at ~£3.41 billion EasyJet’s pre-2026 peak market cap: Approximately £6 billion (2019) EasyJet’s share price fall in 2026: Down approximately 20% year-to-date before bid announcement EasyJet’s fall from 12-month peak: Down approximately 40% from 12-month high before announcement FTSE demotion: EasyJet relegated from FTSE 100 to FTSE 250 in March 2026 June 26 hard deadline: 5:00 PM London time — Castlelake must bid or walk away EasyJet board response: “Highly opportunistic” — will consider any formal proposal Barclays sum-of-parts valuation: More than £11 per share — fleet + slots + Holidays division Deutsche Bank note (Rowbotham): EasyJet fleet, margin gains and gateway airport positions cited as key value drivers Stelios Haji-Ioannou stake: ~15% concert party — brand royalty of 0.25% of revenues complicates any deal EU ownership rules: Maximum 50% non-EU ownership for an EU-licensed carrier — structural hurdle for Castlelake Fleet: 355 aircraft — A319, A320, A320neo, A321neo — 86% owned outright Net book value of owned assets: £5 billion — aircraft alone worth more than the entire market cap Routes: 1,207 routes · 38 countries · 164 airports Key slot positions: London Gatwick · Paris Orly · Geneva · Amsterdam · Berlin · Milan EasyJet Holidays: Growing package holidays division — material standalone value Previous Castlelake airline involvement: Spirit Airlines (talks, did not proceed) · SAS stake (sold to Air France-KLM) Castlelake AUM: ~$36–37 billion Brookfield AUM: ~$365 billion (total credit platform including Oaktree, Primary Wave) Loss for H1 FY2026 (6 months to March 2026): €638 million — vs €456 million same period prior year Fuel surcharge impact on losses: Higher fuel costs added ~€29 million to H1 losses Medium-term profit target: EasyJet’s own target — £1 billion+ annual pre-tax profit

Nine days. That is all the time left before one of the most watched deadlines in British corporate aviation history expires. At 5:00 PM on Friday June 26, 2026, Castlelake — a Minneapolis-based investment firm majority owned by Brookfield Asset Management and managing $37 billion in assets — must either announce a firm intention to bid for easyJet, or formally walk away under UK Takeover Code rules. The minimum price on the table is 403 pence per share — valuing Europe’s second-largest budget airline at £3.06 billion. The announcement sent easyJet shares 13% higher in a single session. EasyJet’s board called the approach “highly opportunistic.” Analysts at Barclays said the airline’s parts are worth more than £11 per share — nearly three times the minimum bid price. Stelios Haji-Ioannou, the airline’s founder, holds a 15% stake and a 0.25% revenue royalty that complicates any transaction. EU ownership rules create a structural hurdle for any non-European buyer. And the airline itself is losing €638 million in the first half of its financial year. Here is everything passengers, investors and aviation watchers need to know about the most consequential airline deal in Europe in 2026.

Understanding the Castlelake bid requires understanding what happened to easyJet’s valuation in the twelve months before the approach was disclosed.

2024: EasyJet sits in the FTSE 100 with a market capitalisation approaching £6 billion. The post-COVID recovery is generating strong passenger numbers. The airline is growing its easyJet Holidays package business as a higher-margin revenue stream. The outlook is cautious but constructive.

Late 2025: The Iran war begins escalating following the US-Israeli military strikes. Jet fuel prices — which had stabilised around $99 per barrel — begin rising. Passenger confidence on Middle East routes softens. EasyJet’s share price begins declining as investors reassess the fuel cost outlook.

January–March 2026: Jet fuel hits $142 per barrel — a 44% increase from pre-conflict levels. EasyJet’s H1 FY2026 results show losses of €638 million for the six months to March 2026, up from €456 million in the same period the prior year. Higher fuel costs alone add approximately €29 million to the figure.

March 2026: EasyJet is relegated from the FTSE 100 to the FTSE 250 as its market capitalisation falls below the index threshold. FTSE demotion forces mandatory selling by index-tracking funds, depressing the share price further.

May 29, 2026: Castlelake publicly discloses it is in the “early stages of considering a possible offer” for easyJet. The disclosure triggers a formal possible offer period under UK Takeover Code rules.

June 1, 2026: Castlelake files a further announcement disclosing it already holds 2.14% of easyJet’s ordinary shares. It states any offer would be at no less than 403.23 pence per share.

June 1, 2026: EasyJet board responds. It describes the approach as “highly opportunistic” — but crucially states it will consider any formal proposal.

June 1, 2026: EasyJet shares trade as high as 449.9 pence — up 13% from the prior close — as the market prices in the probability of a formal bid.

June 26, 2026 at 5:00 PM: The hard deadline. Castlelake must bid or walk.

Castlelake is not a household name. It is a specialist private credit and alternative investment firm based in Minneapolis, Minnesota, managing approximately $36–37 billion in assets across private credit, aviation finance, consumer lending, commercial real estate and small business lending.

Its aviation credentials are extensive and directly relevant to an easyJet bid:

SAS Scandinavian Airlines: Castlelake previously held a significant stake in SAS during its restructuring period and subsequently sold its position to Air France-KLM. It knows European airline workouts from the inside.

Spirit Airlines: Castlelake held discussions about a possible offer for Spirit Airlines — the US ultra-low-cost carrier that eventually ceased operations on May 2, 2026 — but did not proceed. The Spirit talks demonstrated Castlelake’s appetite for distressed airline situations.

Castlelake Aviation: The firm previously operated a dedicated aviation lending and leasing business — Castlelake Aviation Limited — before selling a portfolio of 118 aircraft to Avolon in 2024. It understands fleet values, lease structures and aircraft finance at a level most airline investors do not.

Castlelake is majority-owned by Brookfield Asset Management — the Canadian alternative investment giant with approximately $865 billion in assets under management globally. Brookfield acquired its majority stake in Castlelake in 2024, adding it to a $365 billion credit platform that also includes Oaktree Capital Management and Primary Wave.

The Brookfield connection matters for two reasons. First, it provides Castlelake with access to capital far beyond its own $37 billion platform — a £3 billion easyJet acquisition is financeable within Brookfield’s broader credit infrastructure. Second, Brookfield’s existing aviation finance exposure (through its infrastructure and private equity arms) gives it an institutional understanding of what an airline’s fleet is worth in a break-up or restructuring scenario — which is precisely the analysis that drives Castlelake’s view of easyJet’s valuation discount.

The 403.23 pence minimum price that Castlelake disclosed values easyJet at £3.06 billion. This is a 1.3% premium to where the shares closed on May 30. As takeover premiums go, 1.3% is negligible — it is a floor statement, not a final offer. The question is how much higher a firm bid would need to go to attract shareholder acceptance.

Barclays analyst Andrew Lobbenberg has put a sum-of-parts value on easyJet of more than £11 per share — covering three main asset categories:

The fleet: EasyJet owns 86% of its 355 aircraft outright. The net book value of those owned aircraft is approximately £5 billion — already greater than easyJet’s entire market capitalisation at the time of Castlelake’s approach. Aircraft are real, liquid assets — they can be sold, sale-and-leased-back, or refinanced independently of the airline operation. A buyer acquiring easyJet at £3 billion is effectively getting the airline’s operational business for free, relative to fleet value alone.

The slot portfolio: EasyJet holds some of the most valuable airport slots in European aviation. Its positions at London Gatwick (where it is the dominant carrier), Paris Orly (its French hub), Geneva (its Swiss hub), Amsterdam Schiphol, Berlin Brandenburg and Milan Malpensa are protected infrastructure assets. Gatwick slots alone — one of the world’s most constrained airports — command multi-million-pound values per pair on the secondary market. Deutsche Bank’s Jaime Rowbotham specifically cited easyJet’s “commanding positions at gateway airports including London, Paris and Geneva” as a primary value driver.

EasyJet Holidays: The package holidays division has been growing rapidly as a higher-margin business alongside the core airline. Package holiday margins are structurally higher than airline ticket margins, and the holidays business has its own standalone value as a travel retailing operation. This division is largely invisible in the distressed airline valuation that Castlelake is approaching at 403p — but it represents a material asset for any break-up analysis.

EasyJet said its share price is temporarily depressed by the current Middle East conflict, which has affected both customer confidence and jet fuel prices. That statement is true. It is also exactly why Castlelake moved now.

The Iran war has created a specific, temporary distortion in easyJet’s valuation:

Castlelake’s thesis, in plain terms: easyJet is worth significantly more than its current market price because the factors depressing the price are temporary. A private buyer at £3 billion can wait for the Iran situation to stabilise, fuel costs to normalise, and the underlying value of the fleet and slots to reassert itself — at which point a re-listing or asset sale could return multiples of the entry price.

Sir Stelios Haji-Ioannou, the Greek-Cypriot entrepreneur who founded easyJet in 1995, holds approximately 15% of the airline’s ordinary shares through his family concert party. He also receives a 0.25% royalty on all easyJet revenues for the use of the easyJet brand.

Stelios is not a passive shareholder. He has a long history of public disagreements with easyJet management over strategy, dividends, fleet orders and executive pay. Any takeover of easyJet must either carry Stelios’s support or offer a price high enough that he would accept despite reservations.

The 0.25% revenue royalty is a particularly complex element. Any transaction must consider the interests of easyJet founder Sir Stelios Haji-Ioannou, whose concert party holding controls 15% of the company and receives a 0.25% royalty on revenues for the use of the brand. In a take-private scenario, the royalty arrangement would either need to be bought out — at a price Stelios would accept — or maintained in perpetuity, which affects the economics of any post-acquisition restructuring. At easyJet’s current revenue run-rate of approximately £7 billion per year, 0.25% equates to approximately £17.5 million annually — a material ongoing cost for any acquirer.

European aviation law requires that an EU-licensed airline must be majority-owned and controlled by EU or EEA nationals or entities. EasyJet operates EU-licensed subsidiaries — easyJet Europe Airline GmbH in Austria — that carry the EU operating licence covering its continental European network.

EU ownership rules pose a structural hurdle to any bid, since Castlelake’s investor base is global despite its London and Dublin operations. A Castlelake acquisition that took more than 50% non-EU ownership of easyJet’s EU-licensed entities could technically trigger a review of the EU operating licence — potentially forcing route restructuring or the creation of separate holding structures.

This is not an insurmountable obstacle — multiple European airline groups have navigated complex ownership structures — but it adds legal, regulatory and structural cost to any Castlelake transaction. Castlelake’s legal and structuring team would need to engineer an acquisition vehicle that satisfies both UK Takeover Code requirements and EU aviation ownership regulations simultaneously.

The gap between Castlelake’s stated minimum (403p) and Barclays’ sum-of-parts valuation (more than £11 per share) is enormous — a factor of nearly three. In practical takeover terms:

The most likely outcome if Castlelake proceeds to a formal bid is a price somewhere in the 500p–750p range — a 25–85% premium to the pre-announcement share price — which institutional shareholders might accept while still representing a significant discount to theoretical break-up value.

Castlelake announces by 5pm June 26 that it does not intend to make an offer. EasyJet shares fall back toward pre-announcement levels (approximately 400p). The airline continues as a listed company. No immediate impact on passengers, fares or routes.

Probability: Moderate — the 403p minimum is an opening position, but institutional resistance and the Stelios complication may lead Castlelake to conclude the deal cannot be done at a price that makes financial sense.

Castlelake announces a firm intention to make an offer at a higher price — likely 500p–750p — representing a genuine premium. EasyJet’s board must formally respond. Shareholders vote on acceptance. The process takes 3–6 months minimum.

Probability: Moderate — the strategic logic is sound and the fleet-versus-market-cap discount is real. The question is whether Castlelake can structure a financing package that makes the economics work at the required premium.

A third party — a larger airline group, a sovereign wealth fund, another investment firm — makes a competing offer before June 26 or shortly after. EasyJet’s board uses the Castlelake interest to run a structured sale process.

Probability: Lower but not negligible — Ryanair has historically been interested in easyJet’s slot portfolio, and IAG (British Airways’ parent) has made no secret of its interest in European consolidation. However, competition authorities would likely block Ryanair acquiring easyJet’s Gatwick slots.

Castlelake increases its holding above 2.14% but below the 30% mandatory bid threshold, building a blocking stake or strategic influence position without full acquisition. EasyJet remains listed but with a significant new institutional shareholder on the register.

Probability: Low but possible if the full takeover proves structurally unworkable due to EU rules.

No change to flights, fares or routes. EasyJet continues operating normally. A failed bid might actually benefit passengers — the temporary media and market attention often prompts airlines to improve customer-facing metrics to demonstrate operational strength.

Bookings: All existing easyJet bookings are fully valid. No action required.

The critical passenger question is: what does a private equity owner do with an airline?

Fares: Private equity ownership typically does not reduce fares — in fact, a Castlelake-owned easyJet focused on maximising return on invested capital would likely pursue higher ancillary revenues (baggage fees, seat charges, priority boarding) and potentially reduce capacity on unprofitable routes. Passengers on marginal routes — smaller UK regional airports, less-trafficked European destinations — could see reduced service.

EU regulation: Any Castlelake acquisition would likely maintain easyJet’s EU licence through a restructured holding entity — the European network is too valuable to sacrifice. Passengers on EU routes should expect continuity of service through any ownership change.

EasyJet Holidays: The holidays division is one of the highest-value assets in any sale. A new owner is unlikely to sell or shut down the holidays business — it is more likely to invest in it as a margin-expansion opportunity.

Existing bookings: Under UK consumer law, all booked flights must be honoured by any new owner. A change of ownership does not void existing bookings. All EU261/UK261 passenger rights are maintained regardless of who owns the airline.

Routes and slots: The Gatwick, Orly and Geneva slot portfolios are the most valuable assets in any acquisition. A rational buyer preserves these — they are the core of easyJet’s competitive moat. Route cancellations following a takeover would reduce the value of the assets being acquired.

Nothing urgent. This is a possible offer period, not a confirmed takeover. EasyJet is operating normally. Bookings are valid. Flights are running (subject to the ongoing 78-day disruption crisis and the Paris CDG strike tomorrow).

If you have concerns: EasyJet holds an investment-grade credit rating and a net cash position — it is not at risk of imminent financial failure. The Castlelake bid is a valuation story, not a financial distress story. There is no Monarch Airlines or FlyBe situation here.

If you want to hedge: If you are booking future easyJet travel and have concerns about a potential ownership change, book with a credit card that provides Section 75 protection (UK consumers) or use a travel insurance policy that covers airline insolvency (which this is not, but belt-and-suspenders).

| Date | What to watch |

|---|---|

| June 17–21 | Any Castlelake regulatory filings indicating position changes |

| June 18–20 | Any institutional shareholder commentary (major funds indicating support or opposition) |

| June 21–24 | Stelios Haji-Ioannou public statements — his position is the clearest signal of bid viability |

| June 25 | Final trading day before deadline — share price indicates market expectation |

| June 26, 5pm | THE DECISION: Bid or walk. No extensions without Takeover Panel consent |

More than any analyst note or investor call, the clearest signal of whether this bid can succeed is what Sir Stelios says publicly before June 26. He has made his views on easyJet management known publicly many times before. If he signals openness to a sale at the right price, a Castlelake formal bid becomes much more viable. If he signals opposition, the 15% blocking position makes it near-impossible for Castlelake to reach the acceptance threshold without his cooperation.

Watch: easygroup.com (Stelios’s holding company) and any statements to the London Stock Exchange from the easyJet concert party.

| Metric | Data |

|---|---|

| Fleet size | 355 aircraft |

| Aircraft types | A319 · A320 · A320neo · A321neo |

| Fleet ownership | 86% owned outright |

| Fleet net book value | ~£5 billion |

| Routes operated | 1,207 routes |

| Countries served | 38 |

| Airports served | 164 |

| Key slot positions | London Gatwick · Paris Orly · Geneva · Amsterdam · Berlin · Milan |

| Passengers per year | ~90 million (FY2025) |

| Employees | ~17,000 |

| IATA code | U2 |

| Stock exchange | London Stock Exchange (LSE) — FTSE 250 |

| Ticker | EZJ |

| Minimum bid value | 403.23p / £3.06 billion |

| Barclays sum-of-parts | £11+ per share / ~£8.4 billion |

| June 26 deadline | 5:00 PM London time |

Posted By : Vinay

Lastest News

2nd Floor, 39, Above Kirti Club, DLF Industrial Area, Kirti Nagar, New Delhi, Delhi 110015

Travel Tourister is a leading Travel portal where we introduce travellers to trusted travel agents to make their journey hasselfree, memorable And happy. Travel Tourister is a platform where travellers get Tour packages ,Hotel packages deals through trusted travel companies And hoteliers who are working with us across the world. We always try to find new and more travel agents and hoteliers from every nook and corners across the world so that you could compare the deals with different travel agents and hoteliers and book your tour or hotel with the one you have chosen according to your taste and budget.

Copyright © Travel Tourister, India. All Rights Reserved

Call

Call Enquiry

Enquiry